Written by Christoffer O. Hernæs at his personal blog about Innovation, Finance and Technology: Hernaes.com

Open banking: An introduction

The landscape for financial services is changing, and the jury is still out on how the endgame is going to play out. However, one of the concepts that are starting to stand out as inevitable is open banking. This development emerges out of a perfect storm of shifting customer behavior, regulatory changes, the threat from digital ecosystems such as Google, Apple, Facebook and Amazon, and the quest for new business models are driving banks toward open banking.

The coming European payment service directive, PSD2 is requiring banks to open up the payment infrastructure to third-party providers. New business models based on a platform economy is threatening existing revenue streams. As an example, the P2P lending industry is seeing significant growth, especially in developed countries with strong financial markets. In 2015, the alternative finance industry in the US grew to $36.49 billion, a 212% annual increase from the $11.68 billion in 2014. Europe is also catching on, the total European alternative finance market grew by 92% to reach €5.43 billion in 2015.

There is no need to ask what will be the Uber of banking. The Uber of banking is Uber. 30% of Uber drivers in the US have never had a bank account, but is instead allowing drivers to easily register for a bank account (through integration to a bank partner) or prepaid card when signing up to work for Uber, according to the documents. By doing so, drivers can be paid the same day they work instead of weekly or monthly. Effectively making Uber the fastest-growing acquirer of small business accounts in the US.

This shows that industry boundaries are blurred in the digital world. The payment service M-Pesa by Vodaphone and Safaricom has 18 million customers and more than 80 000 agent outlets, financial services account for 9 percent of Telecom operator Telenor’s total revenue in Pakistan. Customer expectations shaped by digital ecosystems differ from the traditional approach to digital marketing where the dominating logic has been to bring customers to the company’s website or proprietary application platform. Citi research refers to this development of contextual commerce, where a technology/platform enables a consumer to interact and transact with their chosen merchant/brands in the consumers preferred context or medium.

New technology if shifting the center of gravity for traditional core banking systems. A blockchain-based approach to core banking could act as a catalyst to fracture the monolithic and vertically integrated approach to core banking. A modular approach to lending, syndication, capital markets could utilize blockchain to tie it all together. All the other elements of transactions management, the integrity of transactions, messaging, etc. are inherent features of blockchain. Banks cannot afford to ignore the internet of things. When machines are able to perform transactions with machines in real-time at a marginal cost basis, the concept of payments will become obsolete in many use cases as transactions become automated and integrated into other platforms and services. As paying for an Uber today is hidden for the end-customer, the self-driving car of tomorrow could perform payments to the charging station on its own behalf.

These trends all sum up to the inevitability of open banking or banking as a platform.

However, open banking should be perceived as more than just a technical implementation. For banks to embrace open banking, incumbents need to also challenge internal culture and existing business models. Spanish bank BBVA has been a pioneer in this field together with Fidor, and banks like Capital One, ABN Amro and Nordea are all joining the open banking revolution. While open banking may not be the silver bullet for reinventing banking industry, it represents a catalyst for change.

APIs are at the heart of open banking. If executed correctly propose to increase innovation, foster collaboration, extend customer reach and lower costs compared to existing legacy systems. A key concept in the open banking paradigm is to use open source technologies to enable third-party developers to build financial applications on top of the banks’ existing infrastructure. This will most likely spark fears of becoming a commodity and giving away the customer interface for many bankers and may seem like the banks will be relegated to the back seat while third-party technology companies are driving the car.

When I started working in banking, my job was to prevent that from happening. Now I am strongly advocating that if the customer wants it, the back seat is probably the best place for banks as long as it is done willingly. After all, there is a vast difference between choosing to chill out in the back seat and being forced to.

With this, I wish to go more in-depth of the key concepts of open banking in the next series of posts covering various topics related to open banking.

The nature of digital ecosystems

It is impossible to address the subject of open banking without looking at the nature of digital ecosystems. While regulatory changes may act as a catalyst for open banking, the growth and nature of digital ecosystems are in my opinion the primary driving force behind the open banking paradigm.

The banking industry is facing many of the same perils as the telco and media industry has been through in the latter years, and the primary challengers are the same ones that have been feasting at the media and telco’s profit margins for more than a decade. These are the four horsemen of the incumbent’s apocalypse (Google, Apple, Facebook, and Amazon). While they are vastly different in many ways, they all share the traits of a successful digital ecosystem.

Every digital ecosystem starts out as a digital platform, and according to World Economic Forum, the platform economy is expected to disrupt all, or certainly, most existing industrial sectors while stimulating the birth of many new ones. According to Irving Wladawsky-Berger of MIT, a platform or complement strategy differs from a product strategy in that it requires an external ecosystem to generate complementary product or service innovations and build positive feedback between the complements and the platform. The effect is much greater potential for innovation and growth than a single product-oriented firm can generate alone. Scale increases the value of a digital ecosystem, helping it attract more complementary offerings, which in turn brings in more users and increase the value of the ecosystem. A successful digital ecosystem manages to repeat this process.

Napster may have challenged the status quo for the record industry, but it was neither the .mp3 file-format nor the iPod that disrupted the physical music distribution. It was when Apple created a seamless digital ecosystem for digital music consumption through iTunes things started to change. However, as the world progress, yesterday’s innovations become today’s museum pieces, and streaming is already rendering digital music download obsolete. So far, Spotify is excelling at this game, and one of the reasons is their ability to utilize big data analytics and social connections to create a unique personalized listening experience. The ability to create collaborative playlists and connect with your friends through Facebook gives Spotify a competitive advantage over competing services by leveraging third-party access to Facebook’s digital ecosystem.

Facebook stands out as one of the foremost examples of a well-executed digital ecosystem. Starting out as a social network, Facebook has evolved into a digital ecosystem and something similar to an operating system for your digital identity. Facebook has probably realized this a long time ago and allows fragmentation of the front-end by leaving both Instagram and WhatsApp as separate applications. When it comes to user engagement, Facebook’s reigns supreme above all others. WhatsApp has exceeded 1 billion users, and Facebook Messenger also reports more than a billion users, handling 60 billion messages a day combined — three times the number of traditional text messages. The result is a separation of Facebook messenger from the Facebook content platform as a separate platform

A digital ecosystems horizontal integration should also include both customers, partners and third-party services. Facebook caters to brands and agencies that wish to take advantage of Facebook’s vast user penetration though Atlas and Pages Manager.

At the same time, Facebook allows third-party developers to create apps and services through Facebook for developers for the Facebook content platform as well as encouraging everyone to create third-party apps as chatbots on the messenger platform. Allowing co-creation and open innovation, while ensuring data collection through Facebook Connect.

Amazon recently updated its API Gateway service to include Usage Plans. Usage Plans allow Amazon API Gateway customers to regulate and monetize their own APIs through different levels of access and different categories of users. In addition, Amazon also opened up Alexa’s APIs.

An important trait by successful digital ecosystems is their ability to cater to third parties as well as platform owners. Had it not been for the existence of such ubiquitous platforms like Android and iOS as well as Google Maps for its core functionality in addition to Google Play and Apple’s App Store for distribution it is difficult to imagine how Pokémon Go could have achieved the scale and success we witnessed earlier this year.

A successful digital ecosystem is often based on a core engine or business model. However, as the external environment is changing, so has the center of gravity for digital ecosystems pivoted accordingly?

iTunes reigned supreme as the center of Apple’s ecosystem, but the iPhone required another core engine. This transition birthed the app store as the new core in Apple’s digital ecosystem. Google has gone through the same evolution from AdWords and AdSense to the Android platform with Google Play as the center for third party engagement. Amazon has also successfully pivoted from the traditional marketplace as core to Amazon Web Services, which is now Amazon’s most profitable segment. Facebook is still rooted in the user’s digital identity, however, acknowledging shifting user behavior and increasing focus on the messenger platform.

When facing disruptive innovations, digital ecosystems are powerful offensive tools. It was not the iPhone who killed Nokia, it was the app store. In the age of digital ecosystems, it is important to find one’s position. I strongly discourage attempting to be Google if you are not Google.

Introduction to APIs

In order to fully grasp the business potential of open banking, it is useful to have some insights into the technical concepts defining the open banking paradigm. This is meant to be a short introduction to APIs for non-technical people. There are over 12,000 APIs offered by firms today, according to programmableweb. Salesforce.com generates 50% of its revenue through APIs; Expedia.com generates 90%, and eBay, 60%.

An API is in its simplest form a standardized protocol for computer programs to talk to each other and is integral to modern software development. The use of APIs range from web-based APIs, operating systems, databases, hardware, or software libraries.

An API specifies the connection mechanism, the data, and functionality that are made available and what rules other pieces of software need to follow to interact with this data and functionality. Although have been used to link software components within an organization along, the Internet has given rise to the popularity of external web-based or public APIs. An organization can use a public API to allow third parties to access their data or services in a controlled environment. Using an API means that only desired aspects of software functionality are exposed, while the rest of the application remains protected. A Facebook ‘like’ on a third party website and an embedded YouTube video are typical examples of the use of public APIs.

In addition to the examples mentioned above, companies such as Google, Apple, and Facebook have created their digital ecosystems through the use of public APIs. BY allowing third parties to add functionality to their core offering, these companies become platforms for third-party innovation. Besides driving revenue, it also shortens time to market through crowdsourcing and co-creation of new products and services, as well as service customer needs through customer demand-driven development.

EBA has made a useful overview of the contents of common technical standards in today’s APIs:

Data Transmission: the way the data is transmitted securely. Almost all APIs use HTTP/HTTPS as a transport layer because it is simple and widely compatible, although there are APIs, which can be used over a wider variety of transport protocols.

Data Exchange: the format of the exchanged data. The most common formats are XML and JSON. While XML has slightly more functionality than JSON, the latter is winning in popularity. JSON can be used for most purposes and is less detailed, thus allows for faster exchange and is considered better machine-readable. Some companies offer their APIs in both formats, whilst others only have one format available.

Data Access: access management (who gets access to which data and how is this achieved). There are multiple standards for this; popular ones are SAML and OAuth 2.0. The first is an XML-based framework and is widely used in business-to-business interfacing. OAuth is a framework that originated in the consumer web services world.

API Design: the way APIs are designed. Common standardized design principles for APIs are REST (Representational State Transfer) and SOAP (Simple Object Access Protocol). REST is currently more popular due to its focus on solving issues related to performance, scalability, modifiability, portability, and reliability. Although SOAP is still popular in enterprise environments, it is considered more complex to implement.

APIs allow technology to evolve exponentially and each company to focus on its own developments, integrating whichever services or data it lacks through the most appropriate API supplier in each case. As an example, about 75% of mobile apps resort to some type of internal API to offer information or features to its users.

When it comes to APIs, the level of openness determines potential reach.

- Private APIs: Private APIs are closed APIs, and therefore exclusively accessible by parties within the boundaries of the organization. By definition, these are not considered ‘Open APIs’ in this information paper.

- Partner APIs: APIs that are open to selected partners based on bilateral agreements. Like Private APIs, Partner APIs are exclusively accessible at the discretion of the provider of the APIs. Bilateral agreements on specific data exchanges between for instance a bank and an enterprise resource planning (ERP) software provider is an example of a Partner API.

- Member APIs: This type of API is open to everyone who is a formal member of a community with a well-defined set of membership rules. When becoming a member of such a community the API provider allows access to the community members who comply with community membership rules and regulations. Future PSD2-mandated Account Information and Payment Initiation Services fall into this category as only authorized or registered Third Party Providers (TPPs) can obtain access.

- Acquaintance APIs: This type of Open APIs is inclusive, as they are open to every- one complying with a predefined set of requirements. Developer portals distribute this type of API, which also comes with some form of standardized agreements. Merchant access to point-of-sale (POS) APIs is an example in this category.

- Public APIs: Public APIs are inclusive and can thus be accessed by anyone, typically with some form of registration for identification and authentication purposes.

As software continues its march to transform all industries, lack of connectivity increasingly equates to being broken. If software developers are the new rock stars, then APIs are the instruments.

Developer friendliness as a competitive advantage

Opening up your APIs provides little to no value unless developers actually want to use your APIs. Providing an excellent developer experience crucial to keep your external developer community engaged.

When setting up public APIs, the developer experience should be given the same level of care and attention as your consumer-facing user experience.

Provide a sandbox as a starting point. This is the easiest way to start exploring the magnificent world of open platforms. Create an environment that mirrors your production environment and encourage developers to test out your APIs (as well as taking them for a spin yourself). This is a great way to get developer feedback on API-design in a risk-free environment. Take the lessons learned from your sandbox playtime with you when designing robust APIs for production.

Communicate regularly with your developers. Provide insight on your platform roadmap in order to entice anticipation on what lies ahead. Be transparent on scheduled maintenance as well as unexpected downtime. As your selection of APIs expands, consider offering a sort of marketplace/gallery of available APIs as well as a way to monitor API status.

API governance must be designed with a risk perspective in mind. Appointing dedicated resources with backgrounds from both security and business development in charge of API usage is integral to maintain a balance between risk mitigation and innovation. This relates to both carefully selecting who is given access to your APIs as well as continuous monitoring of potentially suspicious or unexpected behavior. Make liabilities and terms of use unambiguous and easy to understand. Make sure non-lawyers can understand the legal obligations.

The business model should be transparent and easy to understand. Letting developers try before they buy on a freemium basis is preferable when applicable. Don’t be afraid that you are giving away anything for free. The code required to make use of an API is usually more valuable than the unit price of a couple of thousand API-calls anyway.

Good documentation is an absolute. The language should be consistent and provide detailed instructions on how to use your APIs. Do not assume that developers considering your APIs have a certain skill level or prefer specific language. If third-party libraries are required to make use of your APIS, make sure to specify so in the documentation. At the same time, make sure your APIs are responsive enough for those who do not bother to read the documentation and opt for a trial and error approach to programming.

When done right, having powerful APIs can act as a catalyst for growth. As proven by Stripe, the online payment company that can credit much of their success on having APIs that are described as a dream for any developer wanting to build payment processing into their site.

Getting the business model right

APIS are at the heart of open banking. If executed correctly propose to increase innovation, foster collaboration, extend customer reach and lower costs compared to existing legacy systems. A key concept in the open banking paradigm is to enable third-party developers to build financial applications on top of the banks’ existing infrastructure. To succeed with an open banking strategy without rendering oneself obsolete, finding the right business model is imperative.

For banks considering opening their infrastructure, an API strategy should be considered a business strategy, not an IT strategy. Giving away API access free may drive brand loyalty and allow the API provider to enter new channels, but may prove unsustainable over time. If executed properly, free API access may act as a stepping-stone for both direct and indirect business models.

Data exchange is one of the most common API models and is the core of Facebook’s Graph API. For banks pursuing a databased business model, the rule of thumb is to create a two-way data feed where you receive data every time third parties consume the API.

Transaction based models are perhaps the most familiar one for banks and does not differ much from traditional transaction banking services. The main difference in an API context is the way companies like PayPal and Stripe allows third parties to integrate and utilize their services through plug and play APIs, thus reaching out to a broader audience and driving payment volumes.

Charge by call is the most straightforward monetization model, where third parties pay each time a service offered through the API is called. To succeed with this model, your services need to offer a clear value proposition. Before setting up direct monetization models, you should talk to your customers to see if they would be willing to pay for these services and for how much. As an example, the default price per API query for IBM Watson is $0.0025.

Subscription-based pricing for API access could both be fixed or dynamic. A fixed model is straightforward and offers full API access for a fixed monthly cost. A pay as you go approach is more dynamic, where pricing is determined by metered usage. For example, a cloud computing platform’s usage price could be determined by the operating system platform and size of a platform on an hourly basis. Another dynamic subscription model is a tiered model. Developers sign up for and pay for a particular usage tier based on the number API calls over a fixed time. While the cost increases per tier the cost per API, call usually drops. Vertical Resources uses the tiered business model. Prices drop with consuming more volume (API calls), so after analyzing usage over a period, users can adjust their tier.

Freemium is a great way to get started for both API owners and third parties curious to connect and explore and could serve as a stepping-stone towards both subscription-based models as well as charge by API call. In this, model companies offer developers some of their APIs capabilities free and then charge for additional functionality. For example, a web mapping service could allow a low number of calls to be made to the API free and then any additional calls to the API are charged. Adding additional API access to a Premium subscription offers a strong motivator to upgrade to a higher package, as it allows end-users to customize their experience and workflow more easily.

Balance sheet is an important strategic resource for banks opening their APIs to third parties. Many fintechs are seeking bank partners to provide core financial infrastructure for new products and services. This could benefit banks by increasing assets under management, providing deposits for capital requirements as well as the potential for additional interest margins if credit is involved.

Revenue sharing is an option to encourage open innovation and co-creation with third parties. In this model, it is often the third party who is paid based on the popularity of the third party application. A revenue-sharing model offers shared incentives for both API owner and third-party community and should also provide additional scaling incentives.

No matter which model you choose, it all comes down to profitability. One way to measure, the success of your APIs is a simple Average Revenue Per User Model (ARPU) in order to see if an API strategy is worth your while. Finally, yet importantly, the business model must be aligned with the long-term vision and strategic agenda.

Managing operational risk

There’s always a flip side, and opening up comes at a price. Unprotected APIs could provide a back door to data and critical systems open for criminals and individuals with malicious intent.

Without proper security, API weak points can expose customer data, backend system access, and even monetary systems to unauthorized access, opening up for several operational risks to both systems and businesses as a whole.

To put perspective on how difficult API security is, pretty much every major Internet company has had API security problems according to ProgrammableWeb. We may all remember such internet scandals as the Ashley Madison breach, where numerous adulterers were exposed, or when a bug in the Instagram APIsgave hackers accesses to the personal information of high-profile Instagram-users.

These are just two examples of born-digital companies stumbling in the API security department. When McDonalds rolled out its home delivery app, McDelivery (because, what else should they have called it), an API breach resulted in the exposure of personal information for 2,2 million users, including names, email addresses, phone numbers, home addresses and sometimes the coordinates of those homes, as well as links to social media profiles.

With PSD2 on the horizon, banks are told to open up their APIs to third parties, while at the same time the EU’s new data protection regulation, GDPR is setting strict requirements for consumer data protection, including some stiff consequences for those failing to comply with the regulation.

With this in mind, API security is an increasing concern for companies deploying public-facing APIs, as they provide multiple access points to the underlying infrastructure. A study from cybersecurity company Imperva reveals that 69 percent of companies have public-facing APIs which offer a route to the sensitive data behind applications.

One of the key challenges with APIs is that well-documented APIs often provide a roadmap describing the underlying implementation of an application. Logic and data structures that otherwise would be buried deep in a company’s architecture. According to a CA white paper on API security, this can give hackers valuable clues that could lead to attack vectors they might otherwise overlook. APIs tend to be extremely clear and self-documenting at their best, providing insight into internal objects and even internal database structure – all valuable intelligence for hackers.

While there are many attack vectors, a majority of analysts and data security experts point out a couple of top concerns. For casual readers, things might get a bit techy from here.

DDoS attacks are one of the primary concerns for IT leaders. A typical DDoS attack floods a web application with an overwhelming amount of junk requests, forcing the application to eventually crash by overloading the underlying infrastructure. A poorly written API could use up a lot of computing resources if it starts receiving invalid inputs, and Netflix proved this by executing a sophisticated DDoS attack against themselves, resulting in an exploit that turned Netflix own API against itself, proving that security countermeasures should be constantly evolving.

Man in the middle attacks intercept legitimate transactions and exploit unsigned and/or unencrypted data being sent between the client and the server. The average end-users are the number one largest security risk an API can ever have. Thus, you must assume every user is a vulnerability. Implement password strength requirements, session length, and concurrent connection limitations, and even require periodic re-authentication and authorization for continued use. Track usage and account metrics, and respond to any deviation. Assume that even your best user is subject to hijacking and malicious redirection, and plan accordingly.

Parameter attacks exploit the data sent into an API, including URL, query parameters, HTTP headers, and/or post content. This could be performed in numerous ways. Providing an API with unexpected content, repeated requests or knowingly invalid input are all strategies to provoke a system response, providing useful information, which combined with already public API documentation and available metadata provides a blueprint for the underlying architecture. With enough information, hackers can inject the system with everything from executable files, SQL queries or method calls. In order to mitigate this, code quality should be a top priority. Feedback from exception handling and error messages must be written for API usage to prevent access to valuable system information. Validating input parameter and monitoring known parameter attack patterns should be prioritized.

Even if the technical risks are mitigated, API governance must be designed with a risk perspective in mind. Appointing dedicated resources with backgrounds from both security and business development in charge of API usage is integral to maintain a balance between risk mitigation and innovation. This relates to both carefully selecting of who is given access to your APIs as well as continuous monitoring of potentially suspicious or unexpected behavior.

In summary, API security is hard, and even the best have failed at some point. This should act as a cautionary tale for banks eager to dive into open banking territory. Banks are dependent on trust, and safeguarding customer data is integral to maintain that trust.

A playbook for banks and fintechs

After looking into the subject, it is becoming clear that there is no one size fits all open banking strategy. Rather, several tactical moves are being played out by a variety of both banks and fintechs. To conclude this guide to open banking, I will attempt to describe some of the widely applied moves, as well as give some examples of the type of players that are conducting these moves.

Move #1 The API marketplace

Becoming a fintech app store is for many banks the preferred alternative to open but, but still maintain control over customer relationship and customer data. BBVA pioneered this move through their API marketplace and has seen several followers. Nordea recently announced that they would launch a fully-functioning developer portal and community hub as the first iteration of their open banking strategy. The move makes Nordea one of the first movers in the Nordics to openly state their Open Banking vision. This is not limited to big banks, as Starling is launching an API marketplace of their own. Starling’s public API enables third parties to access customer data and build on top of the Starling Platform to create products and services such as chatbots, spending analytics, or connections with the Internet of Things.

Move #2 The account aggregators

The ability to create a unified overview of your bank accounts is for many ones of the key strategic possibilities under the XS2A rule under PSD2. This move needs no further elaboration, as we already see examples of account aggregators like Tink and Spiir, as well as banks collaborating to make PSD2 a reality before the directive comes into effect. In order to succeed in this game, contextually relevant user experience is crucial, and merely presenting aggregated account balances in a retrospective fashion will not make the cut. in order to venture beyond the limitations of PSD2, Sbanken has partnered with Norwegian State Educational Loan Fund in order to present student loan debt as an integrated part of the digital user experience. Having the ability to view outstanding student debt side-by-side with mortgages and other loans gives our customers for the first time the possibility to view their total debt in one place.

As the directive is implemented, this is likely to become the new normal for every online and mobile banking service out there, effectively shifting focus for banks from attempting to be your customer’s main or only bank towards attempting to be your customer’s favorite bank.

Move #3 The independent advisor

Building on the account aggregator, the trusted financial advisor also includes data from other sources such as rewards and loyalty points, utility bills, insurance, the total cost of car ownership. The ability to give a holistic view of everyday finances will further strengthen the customer relationship. Op Financial Group in Finland is following this strategy and has launched an electric car leasing service. Players seeking to follow this move should also be prepared to include competing for products and services from competitors if these are the best solutions for the customer in order to build and maintain trust.

Move #4 Cross-industry collaboration

Hana Financial and SK Telecom in South Korea has formed a joint venture with the goal of developing a mobile financial services platform. The joint venture is aiming to combine SK Telecom’s mobile technologies and big data analytics with Hana Financial Group’s experience in financial products and mobile financial services to build an open fintech ecosystem. When launched, the platform will offer a variety of mobile financial services – such as payments, remittance and asset management through a single mobile app. Norwegian banks and Telenor previously attempted to collaborate on the mobile payment platform Valyou, as well as Polish bank mBank has launched a mobile banking services directed at SMEs in collaboration with Orange.

Move #5 Hackathons/crowdsourcing

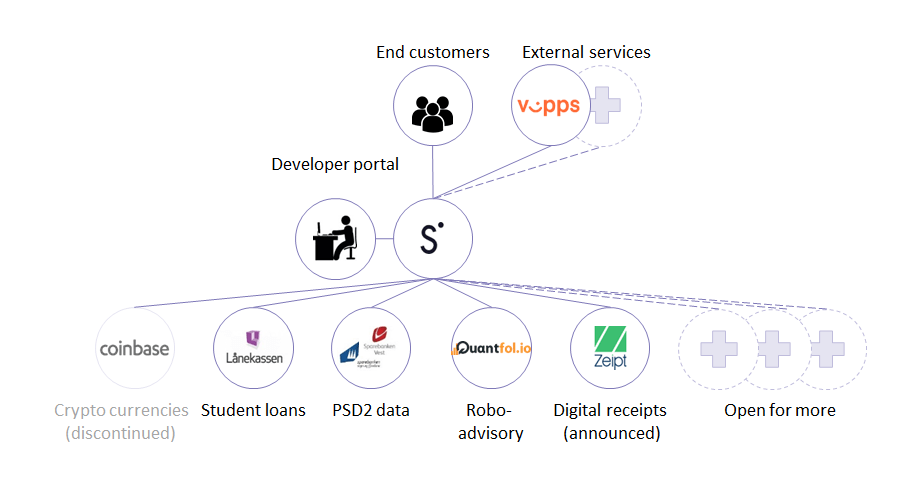

Opening up and allowing approved third parties to build innovative solutions on top of various banks APIs has become a popular choice to test the waters before moving towards the open banking deep end. However, hackathons can also be used beyond simple exploration. ICICI Bank in India is now hosting their second season of their «appathon». The mobile app development initiative offers access of over 250 diverse APIs from both ICICI Bank, IBM Bluemix, VISA and National Payments Council of India to the participants. The program aims to create the next generation of banking applications on mobile and web space by attracting developers, technology companies, start-ups, technopreneurs and students across the globe. In Sbanken we have launched Sbankens developer portal where customers of Sbanken will be able to build their own digital banking services through selected open APIs.

Move #6 Bank/fintech collaboration

Almost every open banking initiative has some element for fintech/bank collaboration. In order to distinguish this as a separate move, I am specifically addressing bilateral collaboration efforts between one single bank and one fintech. The Financial Brand has provided some good examples of how BBVA and Dollar collaborate on payments; USAA collaborates with Coinbase to include cryptocurrencies in their product offerings. At Sbanken we have connected to Quantfolio’s robo-advisor engine to power our robo-advisory offerings.

Move #7 Banking as a service

For many incumbent banks, the idea of becoming a wholesale provider of commodity utilities is considered a worst-case scenario. However, this is absolutely a viable strategic option for some. Germany-based Solaris bank was the first to provide a fully licensed banking platform aimed at fintechs. The platform offers payments, transaction services, deposit and credit services, as well as compliance and KYC/AML solutions. Privatbank in Ukraine is offering a similar service through the Corezoid process engine. Railsbank in the UK is another banking as a service player that provides fintech companies a range of wholesale banking services, including IBANs, receiving money, sending money, converting money, direct debit, issuing cards, and managing credit through APIs.

Move #8 The white label product vendor

Similar to providing the whole bank as a service, some banks and fintechs have collaborated up with the bank as a silent white label provider of products and services that often require a banking license to deliver. Notable examples include Webbank in Utah issuing loans for P2P lenders like LendingClub and Prosper as well as providing lines of credit for Paypal. As a result, Webbank was able to generate a return on equity of 44 percent based on a profit base of only $15,5 million. CBW Bank was also an unknown bank out of Kansas before it was known as the initial bank partner for Moven.

From vision to execution

By now, open banking has become the talk of the town in the banking industry. However, going from strategy to execution is the tricky part. Moving too fast without sufficient understanding your surroundings may result in unforeseen consequences, and on the other hand playing it (too) safe may result in a never-ending strategic analysis of what you could have, would have and should have been done. In order to get started, one must be able to refine and restrict the scope, focus and deliver.

An open banking strategy is in its simplest form centered around two principal roles.

- Integrating third party API to either consume and/or present data or offer third-party services through your platform

- Allowing third parties to consume data and/or build products and services on top of your platform

While most banks are likely to pursue both roles in parallel, a balance between the two is imperative to maintain sufficient focus. This requires a clear understanding of which ecosystem position one is best suited to take. Both in terms of customer value, but also a realistic assessment of prerequisites to take on any given ecosystem role. This includes both internal and external factors such as addressable market size, potential partners, regulatory requirements as well as internal factors such as scale, stakeholder expectations and core capabilities just no name a few.

At the heart of open banking lies your API-platform. Should you build or buy? Next in line is to assess your underlying architecture. Are your core systems fit for fight? How will a potentially exponential increase in API request affect the stability and cost of operations?

Opening up also comes at a price. Unprotected APIs could provide a backdoor to data and critical systems open for criminals and individuals with malicious intent. Without proper security, API weak points can expose customer data, backend system access, and even monetary systems to unauthorized access, opening up for several operational risks to both systems and businesses as a whole.

Do you have a data strategy in place? Hoarding data without purpose increase complexity and diverts attention from utilizing the data already in place.

Governance is equally important. Do your organization have the necessary legal frameworks, onboarding processes, risk assessment procedures, and other control functions in place to handle third-party connections? Following on that note, are they scalable enough?

These are just some of the key questions to make sure you have under control before moving from spreadsheets and powerpoints into the real world.

A good way to get started is to look for low-hanging fruits that may result in tangible actions. I prefer to keep things simple when possible, so I thought I would compile what I called a playbook for open banking based on examples from other banks and financial institutions. There are no lack of case studies on how Facebook, Amazon, Alipay, and Wechat has built vast digital ecosystems around their platforms. While these are fascinating examples, they are not necessarily transferable to your current reality.

One intriguing example was how USAA collaborated with Coinbase to include cryptocurrencies in their product offerings. Not only was this a fairly straightforward integration due to well-documented APIs at Coinbase, but a team of our employees had developed a prototype of the exact same functionality at an internal hackathon. However, simplification was needed to shorten time to market and reduce complexity. Instead of offering a full-fledged digital wallet for cryptocurrencies, we limited the functionality to show the account balance at Coinbase only and chose not to offer any trading possibilities.

After proving our capabilities to integrate third-party functionality, the natural next experiment was to allow third parties to access our APIs. Being customer-driven, the natural next step was to give our customers access to develop their own applications.

If you’re already a customer, sign up at https://utvikler.sbanken.no and get started. If you for some strange reason are not already a customer, customer onboarding only takes a couple of minutes.

Having taken the first step towards open banking it was in good lean startup spirit (build-measure-learn) time to go back to the drawing board with some newly acquired knowledge based on real-world experience.

Even though the technical implementation of PSD2 has been delayed, and Norwegian banks are not required to open up until the second half of 2019, Sbanken, Sparebanken Vest, and Sparebanken Sogn og Fjordane are getting ahead of the curve and are making PSD2 happen long before it is required by entering a collaboration where customers will be able to view their accounts and balance across the competing banks.

We hope to set an example of how banks can collaborate to compete and hope more banks will follow in our footsteps. By doing this now, we are leveraging APIs to create both customer value as well as a competitive advantage rather than waiting until it is required of us to open up our APIs under PSD2.

Last week we followed up by letting customers would view their student loans in our online bank. Having the ability to view outstanding student debt side-by-side with mortgages and other loans gives our customers for the first time the possibility to view their total debt in one place.

By integrating to the Norwegian State Educational Loan Fund through our API-platform, this marks an important step towards giving our customers the ability to make the best financial choices for the future.

The possibilities are vast, and perhaps the biggest challenge is to be able to choose what not to pursue. While open banking today may be perceived as something going on at the side of the existing business, we are approaching an inflection point where we treat open banking as a natural component of banking in a digital age.